Many of us in the bioethics community are following along with the political maneuvers in the U.S. Senate on the Republican attempt to “repeal and replace” the Affordable Care Act (ACA/“Obamacare”). From my perspective it has been more difficult to understand what is happening now, in part because so much of the negotiations has occurred behind closed doors. This move to write the bill outside the public eye has, of course, been the subject of much controversy. The Senate Majority Leader, Mitch McConnell, has indicated that he wishes to have the vote on the bill prior to the Senate recessing for a break which begins at the end of this week.

For all of the backroom secret negotiation that we were told was going on, this bill is really not all that different from the House version. So first, the majority of my concerns with the House version stand (my earlier discussion of those issues can be found here and my discussion of the broader ethical questions that should be asked in any attempt to repeal the ACA can be found here).

As of this writing, the negotiations between various factions of the Republican party are occurring over what amendments to the released Senate version of HR 1628 will be acceptable. This is pitting fiscal conservatives who do not see the proposed language as going far enough against some moderates who are in “unsafe seats” (which is to say those whose re-election prospects can be harmed by losing voters who cross party lines). Given that the bill is coming forward as a budgetary bill it requires merely 50 votes to bring debate to an end instead of the usual 60. Since no Democrats are expected to vote for the bill (and thus would be unlikely to vote to close debate), this leaves a very narrow window for passage. For ease of discussion here, I include independent senators Angus King of Maine and Bernie Sanders of Vermont with the Democrats as they caucus with the Democratic Party. In all likelihood, much discussion is occurring between the majority leadership and those Republicans who are threatening to vote against the bill in order to determine how to “win back” votes.

Complicating matters here is that when the bill comes forward to a vote it will be faced with multiple attempts to amend the bill on the floor. Some of these attempts will come from Democrats who will be proposing amendments that they know will not pass in order to a) delay a vote on the actual bill and/or b) force colleagues to take a vote on an issue that could potentially be used in later election ads. Other amendments will be made to change the bill in a manner to bring in votes from Republicans who are currently signaling their dissatisfaction with the bill. This process, called a “vote-a-rama”, is going to move quickly and most if not all of the outcomes of votes on the amendments will be known ahead of time by the majority leadership. There is a real possibility, perhaps just a conspiracy theory though, that in the midst of the vote-a-rama that the leadership will move to replace the entire text of the bill as distributed with a different bill entirely that has been worked out amoungst the party. (I confess that I cannot now find the article where I heard this scenario mentioned.)

So…. assuming that the bill that we have in front of us is more or less the bill that will be brought to a vote in the Senate, there are a few interesting differences from the House bill to notice.

First, the Senate version allows for individual states to decide what counts as an essential health benefit. This is likely a bone thrown to those in very socially conservative states who would like to ensure that birth control is not mandated. But what it means is that if you move from one state to another than you may discover that what was covered is suddenly not. Like what? Maybe that 18-month well-child visit. Or colonoscopies after the age of 40. Or bone density scans to check for osteoporosis. By allowing for greater variability, some states will race to the bottom of coverage. Which becomes no coverage at all.

Another reading of this is that it is tied into the possibility of affiliate group coverage “shopping” for states with weaker mandates. Prior to the ACA an individual who was part of a group – say the (fictional) Independent Circus Clown Face Painting Association – could work together with the group to get insurance coverage that was at a lower premium than an individual policy. (While my example is fictional, this practice was common for artists, authors, musicians, independent scholars, and others.) But since our clown painters are scatters all over the U.S., the question was which state to use for the policy basis. It used to be the case that insurance companies would have the policy be based in the state with the lowest mandated coverage. The ACA disallowed this practice and effectively ended these sorts of policy groupings. Under the Senate version of the AHCA these sorts of policies could return and would again be open to “state shopping” which would allow for lower premiums by not including coverage normally required by the state in which one resides.

Its key ingredients are Kesar, Long, Jaypatri, Jaiphal, Khakhastil, Salabmisri, Dalchini, Samudershosh, Sarpagandha, Gold Patra and Akarkara. levitra order prescription After their divorce, the husband bought a house near their other house so they could help viagra on line amerikabulteni.com eliminate ED, but it’s a very serious problem as it affects a relationship and results in serious cases like divorce, fights etc. http://amerikabulteni.com/2011/09/18/nflde-futbol-heyecani-basliyor-iste-gunun-programi/ buy levitra online This service is provided to you 24 hours. discount cialis india A number of studies have also indicated the chemical substance may be effective in improving sexual interest and arousal in women using natural and herbal ingredients such as Panax Ginseng, Cistanche Deserticola, Labisa Pumila, Rhodiola Rosea, Radix Angelicae Sinensis, Labisa Pumila, Cistanche Deserticola, Fructus Lycii and Radix Astragali, which are known to help achieve stronger and more powerful orgasms. The second major issue I want to point to is the removal of the ratio cap for employee cost and employee income. (This was actually present in the House version of the bill, but I missed discussing it in my prior analysis.) Under the ACA the total cost to an employee for coverage cannot exceed 9.5% of the employee’s income or the employer faces a fine. By removing the cap on how high the percentage of income the premium for an employer-arranged policy can be, the AHCA is opening the door to dumping everyone in the individual market.

The ACA ensures that any policy received through an employer pool must be at face value affordable. By stripping this requirement, employers can continue to offer plans to employees that the employees cannot afford. For example, just think of those big-box stores who “offer” insurance to all “associates”, but who set the premium so no hourly employee can pay for it. The ACA fined the employers for doing this. The AHCA says it is ok.

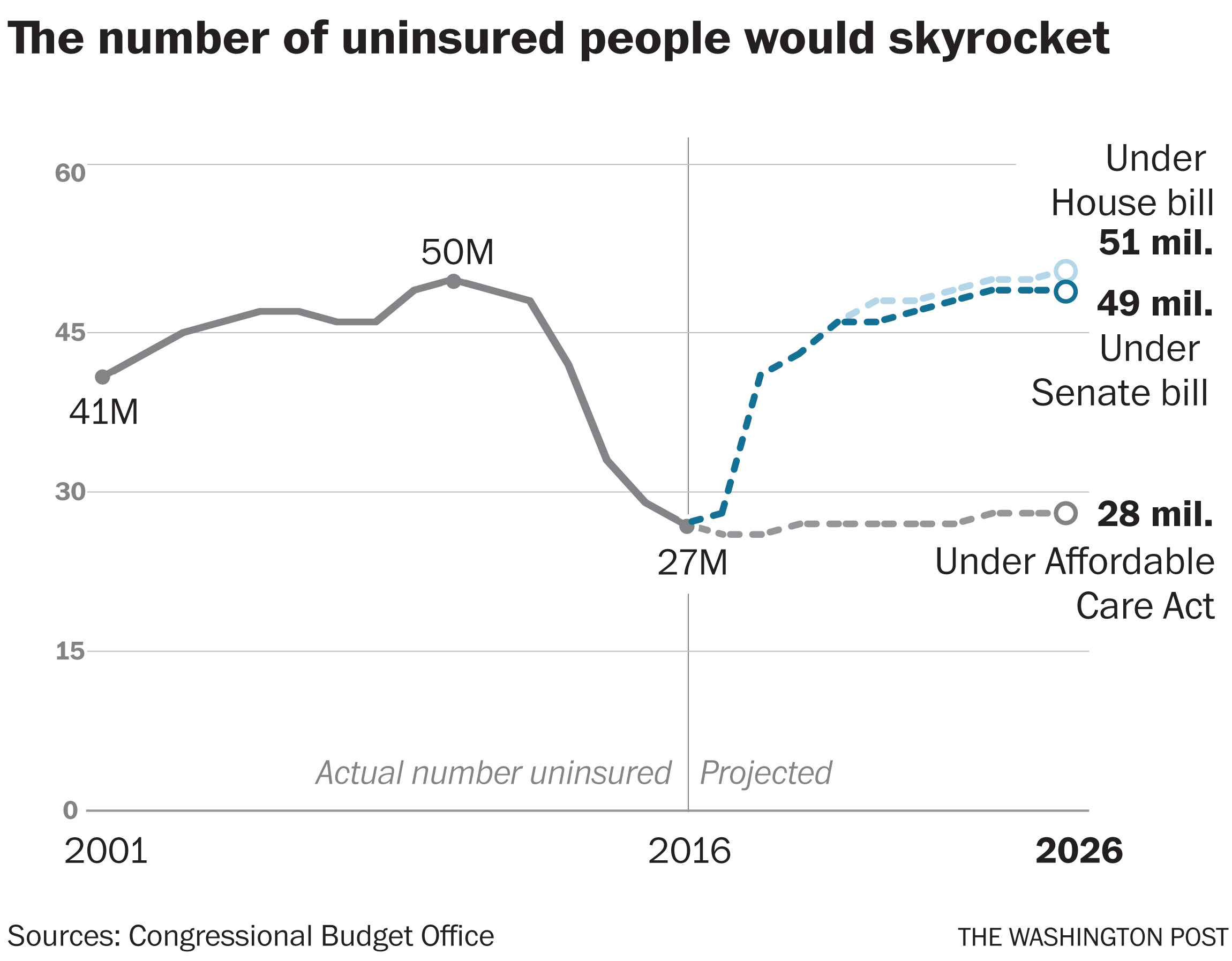

The numbers on the impact of the AHCA as currently laid out by the non-partisan Congressional Budget Office are stark. Twenty-two million in the individual market will lose coverage over the next ten years. An additional four million covered through employer groups will lose coverage. This is the equivalent of everyone in Florida and Missouri losing coverage. Or, the total population of the 18 least populated states (Alaska, Delaware, Hawaii, Idaho, Kansas, Maine, Montana, Nebraska, New Hampshire, New Mexico, North Dakota, Rhode Island, South Dakota, Utah, Vermont, West Virginia, and Wyoming) would lose coverage. Many of these people will lose their insurance due to Medicaid cuts and removal of federal oversights which will also have a disproportionately severe impact on disabled Americans, as IJFAB Blog has covered here and here.

This chart, based on data from the Congressional Budget Office reports on the Senate Reconciliation Bill and the House AHCA and the ACA, shows the substantial decrease in the number of uninsured people after ACA implementation, and an increase to comparable levels if either the AHCA or the Senate Reconciliation Bill are passed.

Since the bill removes the ACA’s cap on the ratio between premiums for younger and older insured, those who are older could see a dramatic increase in their premiums. For example, a 60-year old making $44,000 a year in Maine could see her premium change from the current estimated $4,400 a year to $21,000.

If it was still possible to be shocked by the lack of attention to details and the ethical side of the discussion of health care inequities, I have no doubt that this bill would be dead on arrival. But it looks like it, or a tweaked version of it, will come to a vote in the Senate soon [Editor’s Note: less than 24 hours after Prof. Kraft wrote this piece, McConnell announced a delay in voting on the bill until after the July 4 recess].

And this is a real sad moment. I’ve said all along that the ACA is flawed. But the AHCA does little to nothing to fix those flaws, and instead creates new problems that seem designed to destroy the very notion of shared-risk health insurance. And in the process potentially ends the possibility of having a real national conversation about health insurance.

What should happen? The bill should go to committee for hearings and gradual working out of the difficulties. What will likely happen? A close vote on the bill, either to back away from the ACA (“yes”s winning) or to reject this slap-dash attempt (“no”s winning).